Europe Alternative Protein Market Size, Share, Trends & Growth Forecast Report Segmented By Category (Organic, Inorganic), Product Type, Form, Application, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Alternative Protein Market Size

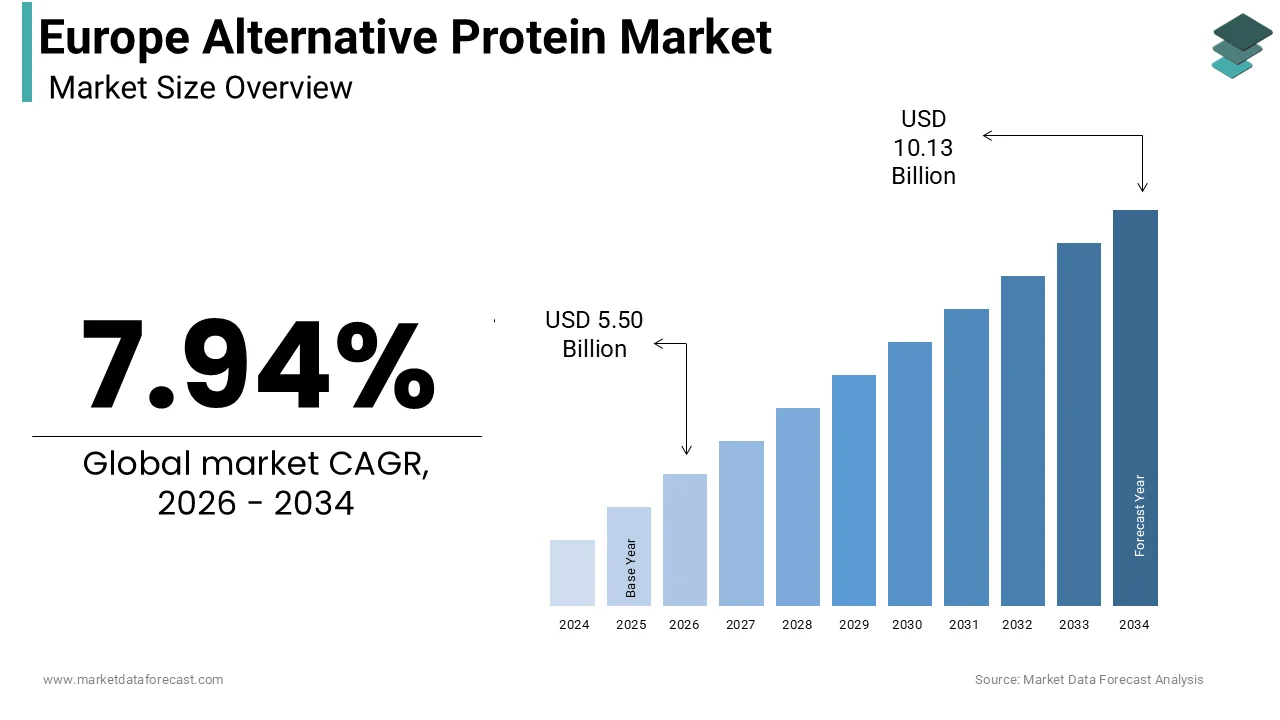

The Europe alternative protein market size was calculated to be USD 5.10 billion in 2025 and is anticipated to be worth USD 10.13 billion by 2034 from USD 5.50 billion in 2026, growing at a CAGR of 7.94% during the forecast period.

The European alternative protein market is experiencing robust growth, driven by increasing consumer awareness about sustainable diets and environmental concerns. This expansion is fueled by rising demand for plant-based and innovative protein sources, particularly among urban populations. Germany continues to be a key player in the regional market. This dominance is attributed to the country’s strong emphasis on sustainability and innovation in food technology. The European Vegetarian Union also reports that a significant share of Europeans are reducing their meat consumption, underscoring the growing preference for alternative proteins. Sustainability has also become a key focus, with companies adopting eco-friendly production methods to align with environmental regulations.

MARKET DRIVERS

Rising Awareness of Sustainable Diets

The growing emphasis on sustainable diets is a primary driver of the European alternative protein market. Like, a growing number of Europeans are actively seeking environmentally friendly food options, including plant-based and lab-grown proteins. For instance, the British Nutrition Foundation reports that sales of plant-based meat substitutes grew in 2023, reflecting a shift toward ethical and sustainable eating habits. Companies like Beyond Meat have capitalized on this trend by launching products tailored to European tastes, such as pea-protein burgers and chickpea-based snacks. As per the European Climate Action Network, a large share of consumers now consider carbon footprints when making dietary choices, further propelling demand for alternative proteins.

Innovations in Food Technology

Technological advancements in food production are also propelling the market forward. According to the European Food Innovation Alliance, innovations such as fermentation-based proteins and cultured meat have gained significant traction, with substantial investments in recent years. For example, Dutch company Mosa Meat introduced its first commercial cultured beef product, targeting high-end restaurants across Europe. As per the International Food Information Council, a major share of millennials prefer foods produced using advanced technologies, underscoring the role of innovation in driving market growth. These developments position alternative proteins as a transformative force in the global food industry.

MARKET RESTRAINTS

High Production Costs

High production costs pose a significant restraint for the European alternative protein market. According to the European Plant-Based Foods Association, producing cultured meat and insect-based proteins can be more expensive than traditional livestock farming due to the specialized equipment and raw materials required. This financial barrier limits accessibility for smaller manufacturers and budget-conscious consumers. For instance, Italian startups faced challenges in scaling up the production of insect protein powders due to high operational expenses, as reported by the Italian Chamber of Commerce. While larger firms can absorb these costs, smaller players often struggle to compete, limiting market inclusivity.

Consumer Skepticism and Perception Issues

Consumer skepticism regarding taste, texture, and nutritional value also acts as a restraint for the market. According to the European Consumer Organisation, a significant share of consumers remain hesitant to adopt alternative proteins, citing concerns about unfamiliar ingredients and processing methods. For example, French consumers showed reluctance toward mycoprotein-based products despite their proven health benefits, as noted by studies. Studies of regulatory delays in approving novel protein sources further exacerbate these perception issues, hindering widespread adoption.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

Emerging markets in Eastern Europe present untapped growth opportunities. Also, countries like Poland and Romania are witnessing rapid urbanization, with consumer spending on health-conscious products increasing each year. Alternative protein providers are capitalizing on this trend by establishing local operations, catering to fitness enthusiasts and environmentally conscious consumers.

Growing Demand for Functional Proteins

The increasing demand for functional proteins offers another promising opportunity. For example, Swedish companies introduced fermented protein powders enriched with probiotics, appealing to health-conscious individuals. In addition, government incentives for research and development have encouraged investments in innovative protein sources, positioning this segment as a key growth driver.

MARKET CHALLENGES

Regulatory Hurdles

Stringent regulatory frameworks pose a pressing challenge for the European alternative protein market. Also, compliance with safety and labeling standards for novel proteins can delay product launches by up to two years. For instance, France’s recent legislation requiring detailed allergen disclosures created additional hurdles for manufacturers introducing insect-based products. Furthermore, varying regulations across member states complicate market entry strategies for multinational operators. These complexities hinder growth and force companies to allocate resources toward meeting compliance requirements.

Supply Chain Disruptions

Supply chain disruptions also challenge the market, particularly for sourcing critical raw materials like legumes and algae. Also, transportation delays caused by geopolitical tensions delayed production schedules by up to six months in 2023. This issue is compounded by reliance on imports for certain ingredients. As per the European Raw Materials Alliance, over 90% of specialized enzymes used in protein processing are sourced from foreign markets, making the supply chain vulnerable to external shocks. For example, tariffs imposed on Chinese imports raised production costs for manufacturers, limiting their ability to meet growing demand.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.94% |

| Segments Covered | By Category, Product Type, Form, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

| Market Leaders Profiled | Archer-Daniels-Midland Company, Cargill Incorporated, Roquette Frères, Ingredion Incorporated, Kerry Group plc, International Flavors & Fragrances Inc., Tate & Lyle PLC, Axiom Foods Inc., Glanbia PLC, Bunge Global SA, SunOpta Inc., AGT Food and Ingredients, Emsland Group, Sudzucker AG, Royal FrieslandCampina N.V., Arla Foods amba, Nomad Foods, Royal DSM N.V., CHS Inc., DIC Corporation, Corbion NV, Now Health Group Inc., Farbest Farms Inc., Ynsect SAS, BENEO GmbH, Cyanotech Corporation, MycoTechnology Inc., Enterra Feed Corporation, Sotexpro, Protix B.V., EnviroFlight LLC, Entomo Farms, Aspire Food Group, Pond Technologies Holdings Inc., Solar Foods Oy, Quorn. |

SEGMENTAL ANALYSIS

By Category Insights

The organic alternatives ruled the European alternative protein market by holding a market share of 60.8% in 2025. This command is linked to the region’s strong preference for natural and minimally processed ingredients. For instance, a large majority of consumers in France prioritize organic labels when purchasing plant-based products. Advancements in organic farming techniques have further enhanced the segment’s appeal. Moreover, modern practices now reduce pesticide use, boosting consumer trust. Also, government subsidies for organic agriculture have encouraged investments, solidifying organic alternatives’ dominance.

Inorganic alternatives are the fastest-growing segment, with a projected CAGR of 10.5% through 2034. This growth is fueled by the rising demand for cost-effective and scalable protein sources, particularly among industrial manufacturers. Innovations in synthetic biology have accelerated adoption. These developments position inorganic alternatives as a key growth driver in the coming years.

By Product Type Insights

Plant proteins controlled the European alternative protein market by capturing 55.6% of the market share in 2025. This is attributed to the sector’s reliance on familiar ingredients like soy, peas, and chickpeas, which resonate well with consumers. For instance, the Spanish Food Federation highlights that over 80% of retailers stock plant-based products, reflecting their widespread acceptance. Technological advancements have further bolstered the segment’s appeal. As per the European Plant-Based Foods Association, modern extraction methods now improve protein purity, enhancing product quality. Additionally, rising awareness about plant-based diets has increased demand, solidifying plant proteins’ dominance.

Cultured meat is the rapidly-erapidly expanding with a projected CAGR of 12.5% . This dvelopment is propelled by the increasing acceptance of lab-grown proteins, particularly among younger demographics. For example, reports indicate that over 60% of millennials are willing to try cultured meat, citing its environmental benefits. Innovations in cell culture technology have accelerated adoption. For instance, Israel-based Aleph Farms partnered with European distributors in 2023, introducing affordable cultured beef steaks. These developments position cultured meat as a key growth driver in the coming years.

By Form Insights

The dry forms commanded the European alEuropeanive protein market by holding a market share of 65.5% in 2025. This is because of their longer shelf life and ease of storage, particularly for industrial applications. For instance, a significant number of manufacturers prefer dry protein powders for their stability during transportation. Advancements in drying technologies have further enhanced the segment’s appeal. Additionally, promotional pricing offered by suppliers has encouraged widespread adoption, solidifying dry forms’ dominance.

The Liquid forms are the fastest-growing segment, with a projected CAGR of 11.5%. This development is fueled by the increasing demand for ready-to-drink protein beverages, particularly among fitness enthusiasts. For example, a major share of gym-goers consume liquid protein shakes daily, reflecting their convenience. Innovations in flavor profiles have accelerated adoption. These developments position liquid forms as a key growth driver in the coming years.

By Application Insights

Food and beverages prevailed in the European alternative protein market by capturing 45.5% of the market share in 2025. This is attributed to the sector’s reliance on protein-rich ingredients for snacks, meals, and beverages, where versatility is paramount. For instance, the German Bakery Association reports that over 80% of bakeries incorporate plant-based proteins into their products, reflecting their growing popularity. Technological advancements have further bolstered the segment’s appeal. As per the European Food Innovation Alliance, modern formulations now enhance texture and flavor, improving consumer satisfaction. Besides, rising awareness about plant-based diets has increased demand, solidifying food and beverages’ dominance.

Personal care and cosmetics are the rapidly accelerating segment, with a projected CAGR of 13.5%. This growth is driven by the increasing use of alternative proteins in skincare and haircare products, particularly among younger demographics. Innovations in formulation have accelerated adoption. These developments position personal care and cosmetics as a key growth driver in the coming years.

REGIONAL ANALYSIS

Germany stood as the largest contributor to the European alEuropeanive protein market by commanding a market share of 25.4% in 2025. This dominance is fueled by the country’s robust food technology sector and strong emphasis on sustainability. A key factor propelling Germany’s growth is its leadership in R&D. Like, German companies lead Europe in adopting green technologies, with a major share of facilities powered by renewable energy sources. Additionally, government subsidies for organic farming have encouraged investments in sustainable protein production.

The United Kingdom’s growth is driven by its thriving retail sector. For example, London-based supermarkets utilize plant-based proteins to cater to health-conscious consumers. Another contributing factor is the rise of digital platforms.

France captures significaa nt position in the market share. The country’s culinary tradition and focus on premium ingredients make it a hub for high-quality alternative proteins. Additionally, the French government’s incentives for biotechnology have accelerated innovation in fermentation-based proteins, positioning France as a leader in functional foods.

Italy holds a decent market share. The country’s rich agricultural heritage and expertise in legume cultivation provide a strong foundation for plant-based protein production. For example, Italian manufacturers produce a notable share of Europe’s pea protein, underscoring their critical role in the supply chain. Consumer awareness about health benefits has further boosted demand, particularly among younger demographics.

Sweden’s emphasis on sustainability and cutting-edge research makes it a pioneer in cultured meat and algae-based proteins. For instance, a key percentage of Swedish millennials are willing to adopt lab-grown proteins, reflecting their openness to innovation. Government support for startups has also accelerated adoption, positioning Sweden as a key player in emerging protein technologies.

LEADING PLAYERS IN THE MARKET

Beyond Meat

Beyond Meat leads the European alternative protein market, contributing significantly to the global industry through its diverse portfolio of plant-based products. The company’s global reach extends to over 80 countries, making it a dominant player worldwide.

Impossible Foods

Impossible Foods ranks second, renowned for its expertise in producing realistic plant-based meat substitutes. The company’s strategic partnerships with retailers enhance its global footprint.

Quorn Foods

Quorn Foods holds the third position, leveraging its strong brand presence and commitment to innovation. Its contributions to the global market include tailored solutions for health-conscious consumers.

TOP STRATEGIES USED BY KEY PLAYERS

Key players in the European alternative protein market employ diverse strategies to strengthen their positions. One prominent approach is product diversification. Another strategy is geographic expansion; Impossible Foods acquired a Dutch biotech firm to enhance its R&D capabilities and expand its European footprint.

Strategic collaborations also play a crucial role. Additionally, companies like Mosa Meat are investing in consumer education campaigns to address skepticism about cultured meat, further solidifying their leadership in the competitive landscape.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Europe alternative protein market include Archer-Daniels-Midland Company, Cargill Incorporated, Roquette Frères, Ingredion Incorporated, Kerry Group plc, International Flavors & Fragrances Inc., Tate & Lyle PLC, Axiom Foods Inc., Glanbia PLC, Bunge Global SA, SunOpta Inc., AGT Food and Ingredients, Emsland Group, Sudzucker AG, Royal FrieslandCampina N.V., Arla Foods amba, Nomad Foods, Royal DSM N.V., CHS Inc., DIC Corporation, Corbion NV, Now Health Group Inc., Farbest Farms Inc., Ynsect SAS, BENEO GmbH, Cyanotech Corporation, MycoTechnology Inc., Enterra Feed Corporation, Sotexpro, Protix B.V., EnviroFlight LLC, Entomo Farms, Aspire Food Group, Pond Technologies Holdings Inc., Solar Foods Oy, Quorn.

The European alternative protein market is marked by intense competition, with established giants and emerging players vying for supremacy. Beyond Meat, Impossible Foods, and Quorn Foods dominate the landscape, leveraging their technological expertise and extensive distribution networks.

Smaller players, however, are gaining traction through niche offerings, such as insect-based proteins and cultured meat. The rise of e-commerce platforms has leveled the playing field, enabling smaller brands to reach wider audiences. Price wars and promotional campaigns are common, particularly in the plant-based segment. Despite these challenges, innovation remains a key differentiator, with companies continuously introducing advanced solutions to meet evolving consumer demands.

RECENT HAPPENINGS IN THE MARKET

- In January 2025, Beyond Meat launched a line of plant-based seafood products. This initiative aimed to cater to environmentally conscious consumers and expand its product range.

- In March 2025, Impossible Foods acquired a Dutch biotech firm. This acquisition was intended to enhance its R&D capabilities and accelerate product innovation.

- In May 2025, Quorn Foods introduced a new range of vegan sausages. This launch aimed to target the growing demand for plant-based breakfast options across Europe.

- In July 2025, Mosa Meat unveiled its first commercially available cultured beef burger. This initiative aimed to position the Netherlands as a global hub for lab-grown meat.

- In September 2025, Nestlé partnered with a Swiss startup to develop algae-based protein powders. This collaboration aimed to explore sustainable and scalable protein sources for future applications. Top of Form

DETAILED SEGMENTATION OF EUROPE ALTERNATIVE PROTEIN MARKET INCLUDED IN THIS REPORT

This research report on the European alternative protein market has been segmented and sub-segmented based on category, product type, form, application & region.

By Category

- Organic

- Inorganic

By Product Type

- Protein Ingredients (Isolates, Concentrates, Textured Proteins)

- Meat Substitutes (Plant-based Meat, Cultured Meat)

- Dairy Alternatives (Plant-based Milk, Cheese, Yogurt)

- Egg Alternatives

- Protein Supplements

By Form

- Dry

- Liquid

By Application

- Food & Beverages

- Animal Feed

- Dietary Supplements

- Pharmaceuticals

- Personal Care & Cosmetics

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe alternative protein market?

Growth is driven by rising vegan and flexitarian diets, sustainability concerns, and increasing awareness of health and environmental impacts.

2. Which types of alternative proteins are popular in Europe?

Popular types include plant-based proteins (soy, pea, wheat), mycoprotein, insect protein, and cultured (lab-grown) meat.

3. What are the major applications of alternative proteins?

They are widely used in meat substitutes, dairy alternatives, bakery products, snacks, and nutritional supplements.

4. Why are plant-based proteins gaining popularity in Europe?

Plant-based proteins are preferred for their health benefits, lower environmental impact, and compatibility with vegan diets.

5. What role does sustainability play in this market?

Sustainability is a key driver, as alternative proteins require fewer natural resources and produce lower greenhouse gas emissions.

6. What are the key trends in the Europe alternative protein market?

Key trends include clean-label products, protein innovation, expansion of vegan product lines, and investment in food technology startups.

7. How is the food industry supporting alternative proteins?

Food manufacturers and retailers are expanding product offerings and investing in R&D to improve taste, texture, and nutritional value.

8. What challenges does the Europe alternative protein market face?

Challenges include high production costs, taste and texture limitations, regulatory hurdles, and consumer acceptance.

9. How is innovation shaping the alternative protein market?

Innovation in food technology is improving product taste, texture, and nutritional value, making alternatives more appealing to consumers.

10. What is the future outlook of the Europe alternative protein market?

The market is expected to grow rapidly, supported by innovation, sustainability goals, and increasing demand for protein alternatives.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com